![<?echo $_SERVER['SERVER_NAME'];?>](/template/twentyseventeen/skin/images/header.jpg)

Content directory:

New energy vehicle market analysis and future forecast. Consumption structure is changing, and automobile consumption is expected to continue to grow under the policy. At present, the new energy penetration rate of passenger cars is approaching its peak. Battery contradictions and deceptions weaken the future development potential. The new energyization of passenger cars and special vehicles is the trend of the times. The special vehicles are mainly logistics vehicles, and there are some opportunities in the short and medium term. In the long-term, the passenger car is the core force. The carbon quota policy is expected to be introduced, forming a complete system of limit standards + accounting methods + rewards and punishments + points transactions, aiming at the subsidy policy of gradual decline, requiring vehicle manufacturers to produce a certain proportion of new energy vehicles, with management Regulations, fraudulent compensation, 13th Five-Year Plan, and restrictions on purchase policies in some cities to ensure the sustainable development of new energy vehicles. In the future, new energy vehicles will move toward economical vehicle electrification, intermediate-vehicle hybridization, and medium-to-large SUV insertion and hybridization.

The development and outlook of the lithium battery industry. In 2016, China's power lithium battery is growing rapidly relative to 3C lithium battery, and 2017-2020 power battery manufacturers will continue to integrate, mainly in East China. The ternary vitality begins to decline, and the material threshold has main customer thresholds and cost advantages. The price of lithium carbonate entered the bottoming process, and the price of the wet diaphragm was generally stable.

Lithium-ion power battery technology trends and industrial landscape. New energy vehicles are gradually promoted, and the penetration rate of Sanyuan in passenger cars and special vehicles and lithium iron phosphate in passenger cars is improved. This time, Lithium Energy is mainly for power battery foundation, policy and market, key technologies, market status and future. Development and the entire industry chain for in-depth analysis.

Ternary industry chain technology and market analysis (power battery industry chain research). The subsidy policy has been changed from ex ante allocation to post-event liquidation, and there is a retreat to catalyze, which will accelerate the integration of the entire industry, whether it can enter the catalogue, and obtaining subsidies is the key to the logistics vehicle enterprises to gain competitive advantage. The future opportunity is mainly in the positive electrode material. It is the key to improve the energy density. Due to overcapacity, the price competition is fierce, the profit margin is small, and the profit of lithium iron phosphate is high. However, the structural problems still exist, and the supply of high-end batteries is in short supply. The mainstream route of the battery pack is still square and soft package, but it lacks a unified product system and has low production efficiency. At present, it is mainly based on the transition of cylindrical batteries.

Electric vehicle battery system technology. BMS and PACK are the core of the new energy vehicle battery system and an important technical barrier. Layout BMS+PACK core technology, into the battery industry, automotive industry core industry chain, is the future development direction of BMS manufacturers.

Analysis of the value and business model of energy storage in the energy Internet. China's energy and power development process faces a series of problems. The new energy revolution is centered on the energy Internet (ie, Internet + smart energy), and energy storage is the key link to realize the energy Internet. The No. 9 document of Electric Power Reform clearly proposed to vigorously develop distributed energy storage systems, develop power generation market, and open up the electricity sales market. The global energy storage market will reach trillions in 2024 and usher in a blowout. The energy storage technology route is mainly lead-carbon battery. Nandu is the first investment + operation business model. It is similar to contract energy management. It recovers investment and profits from the energy-saving benefits obtained after customers carry out energy-saving renovation, and fills the valley through energy storage. According to the peak-to-valley price difference of the time-sharing electricity price policy, the profit target can be achieved.

Interpretation of the new energy vehicle operation industry chain. The new energy vehicle operation industry chain is divided into upstream vehicle and charging equipment, midstream operation platform and downstream client. In terms of charging piles, the number has increased rapidly, but the problems of low utilization rate and high operating cost have caused 90% of the charging pile operators to make profit. In terms of new energy vehicle operations, lack of charging infrastructure to support, Beijing and Shanghai timeshare leasing market presents two very different competitive landscapes. Spruce's smart "pile-pile" operation model or provide a new round of new energy vehicle aftermarket solutions.

Analysis of the trend of new energy logistics vehicle industry. From 2005 to 2015, the total amount of social logistics in the country increased year by year, and the number of express delivery and express delivery CAGR was high. However, the shortage of supporting facilities, the pressure of traffic and public security, the vicious competition of logistics and transportation, and the contradiction of road rights also became the pain points of the industry.

text

Interpretation of new energy passenger car market

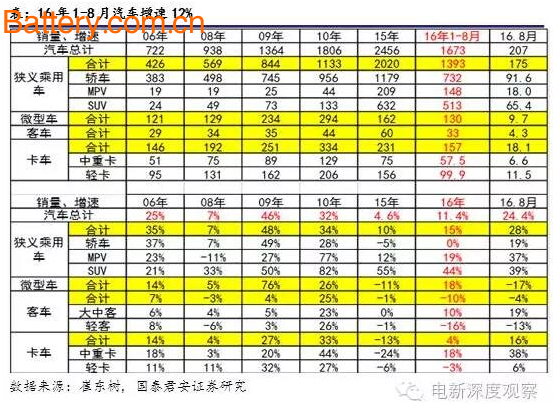

New energy vehicle products - mainly passenger car transfer vehicles. The data of the automobile industry is the highlight of GDP, the consumption structure changes, the automobile consumption ushers in the golden month, and it is expected to continue to grow under the policy push. In the first 16 months of January and August, the growth rate of automobiles was 12%, among which new energy vehicles maintained a relatively fast growth rate. During the 12-15 years, the proportion of passenger cars and special vehicles in the new energy market continued to increase, and the number of passenger cars rose from 19% to 30. %, while the proportion of new energy in passenger cars has reached a high proportion, and the energy consumption of large and medium passengers is 40%, which is close to the peak. Some road passenger transport, tourist buses, school buses, etc. do not need new energy, and it is difficult to export new passenger cars. The 16-year passenger car will become the main growth driver of new energy vehicles.

The driving force of new energy vehicles--subsidy stimulus to mandatory compliance.

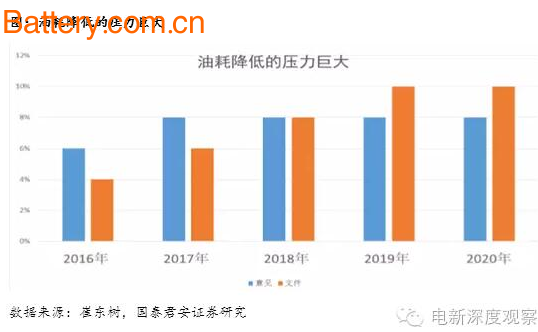

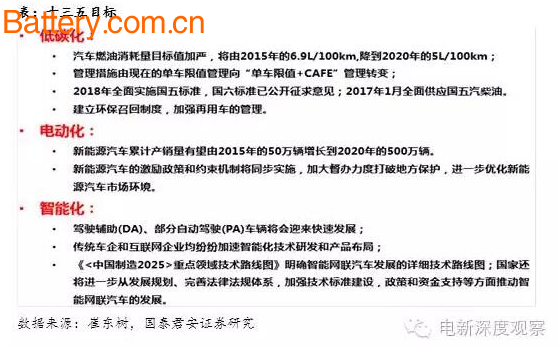

- Carbon quotas are expected to be introduced, in conjunction with the "Living Vehicle Fuel Consumption Limits", "Accounting Methods for Average Fuel Consumption of Passenger Vehicle Enterprises" and "Interim Measures for the Administration of Average Fuel Consumption of Passenger Vehicle Enterprises" to form "Limit Standards + Accounting" The complete institutional system of “method + reward and punishment measures + point transactionâ€. In 2018, the vehicle emission standard V will be fully implemented, and the national VI standard is expected to advance; an environmental recall system will be established to strengthen production consistency and supervision of vehicles in use. The carbon quota is designed to take the subsidy system of gradual decline, and requires vehicle manufacturers to produce new energy vehicles in proportion to the output of traditional vehicles, and continue to guide the steady development of the new energy vehicle market.  - The fuel consumption reward and punishment system is a relatively simple method, but the fuel consumption pressure is relatively small in 16 years. The average fuel consumption index of passenger car companies in 15 years was better than the target of 7%, and the performance of car companies was very good. However, the average annual fuel consumption rate in 12-15 years is less than 3%, far lower than the average annual rate of 8% in 16-20 years. In the future, with the increase of fuel consumption pressure, the supporting new energy subsidy policy will promote the diversified choice of the market, and the hybrid and intermixing of fuel vehicles is the upgrading direction. During the “Thirteenth Five-Year Plan†period, new energy vehicle incentive policies will continue to be introduced, and at the same time, the establishment of a new energy vehicle point management system linked to sales volume will be explored.

- The fuel consumption reward and punishment system is a relatively simple method, but the fuel consumption pressure is relatively small in 16 years. The average fuel consumption index of passenger car companies in 15 years was better than the target of 7%, and the performance of car companies was very good. However, the average annual fuel consumption rate in 12-15 years is less than 3%, far lower than the average annual rate of 8% in 16-20 years. In the future, with the increase of fuel consumption pressure, the supporting new energy subsidy policy will promote the diversified choice of the market, and the hybrid and intermixing of fuel vehicles is the upgrading direction. During the “Thirteenth Five-Year Plan†period, new energy vehicle incentive policies will continue to be introduced, and at the same time, the establishment of a new energy vehicle point management system linked to sales volume will be explored.

- The SUV trend in the narrow passenger car market is obvious, the MPV upgrade trend is faster, and the car market continues to shrink. SUV market segments are frequent and hot to achieve sustainable development.  The demand for new energy passenger cars - the purchase of cities to the national market. From January to August of the year, the total sales volume of new energy passenger vehicles was 180,000 units, an increase of 135% year-on-year. The trend of miniaturization was obvious. The contribution of the city ​​to purchase, the mix of hybrids and electric vehicles was improved, only for licenses and

The demand for new energy passenger cars - the purchase of cities to the national market. From January to August of the year, the total sales volume of new energy passenger vehicles was 180,000 units, an increase of 135% year-on-year. The trend of miniaturization was obvious. The contribution of the city ​​to purchase, the mix of hybrids and electric vehicles was improved, only for licenses and

Policy adjustments ensure the sustainable development of new energy vehicles.

- On March 17th, the government work report proposed that new energy vehicles should focus on electric vehicles , and determine the key directions and key measures for the development of new energy vehicles, including vigorously developing and promoting new energy vehicles based on electric vehicles and accelerating the construction of urban parking lots. And charging facilities. This means that compared with other new energy vehicles (such as FCV), electric vehicles will become the main force in the development of new energy vehicles, and the key problems in the construction of new energy vehicles are expected to be solved.

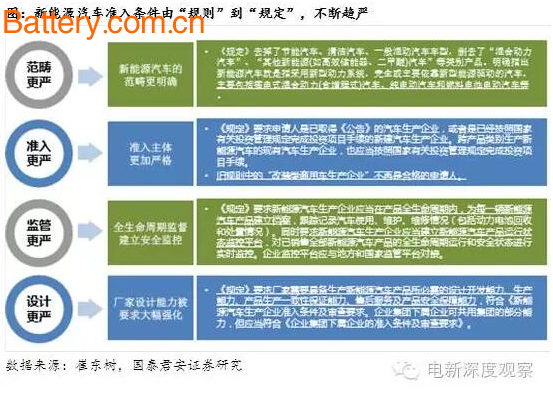

- On January 14th, with the launch of "Road Motor Vehicle Manufacturers and Products (No. 280)", the first batch of new energy vehicle promotion catalogues was launched. The original model of "Recommended Models for Energy Saving and New Energy Vehicle Demonstration and Application Projects" will be abolished from January 1, 2016. This is a major event in the industry, reflecting the new stage of the development of new energy vehicles in the 13th Five-Year Plan. After the launch of the three batches, the new catalogue of new energy vehicles was suspended, waiting for the review of the battery.

- The Ministry of Industry and Information Technology 8.12 "Regulations on the Administration of New Energy Vehicle Manufacturers and Products Access" has a clearer definition of new energy vehicles and applicants compared to the access management rules of 2009, and the access conditions and review of new energy vehicle manufacturers. The requirements are relatively large, and the requirements for new energy auto companies are more clear and specific, making it difficult for independent small and medium-sized enterprises to obtain qualifications. However, at the same time, the “Regulations†have reduced the qualifications of the Group’s subsidiaries for applying for new energy vehicles. Admission conditions favor the existing automobile group. “Strong Hengqiang†or the development trend of the new energy market in the future.

The resulting restrictions will squeeze new energy vehicles into large markets, and Beijing is the standard paradigm.

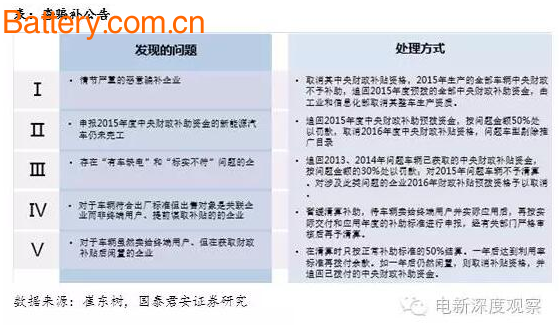

- The sales of new energy in the previous period were poor, and the easing policy was a reasonable choice. At present, the new energy-making effect is super strong, and the external enthusiasm is high and needs to be strictly controlled.

- The Ministry of Finance issued a public disclosure of five typical cases, and detailed the problems and treatments found in this special inspection. After this special inspection, a large probability of welcoming a new energy commercial vehicle subsidy .  - Shanghai issued the “Notice on Supporting the Promotion and Application of New Energy Freight Cars by the Shanghai Municipal Transportation Commission†and the “Notice on Shanghai's Encouraging the Purchase and Use of New Energy Vehiclesâ€, and the supervision of new energy vehicle subsidies extended to products. The entire chain of production, sales and use; Shenzhen issued the "Shenzhen 2016 New Energy Vehicle Promotion and Application Financial Support Policy", the new standard has a large decline in the field of private subsidies, but significantly increased the new energy taxi company Subsidy; Shanxi, Hunan, Jiangxi, Qingdao and other provinces and cities introduced charging infrastructure planning

- Shanghai issued the “Notice on Supporting the Promotion and Application of New Energy Freight Cars by the Shanghai Municipal Transportation Commission†and the “Notice on Shanghai's Encouraging the Purchase and Use of New Energy Vehiclesâ€, and the supervision of new energy vehicle subsidies extended to products. The entire chain of production, sales and use; Shenzhen issued the "Shenzhen 2016 New Energy Vehicle Promotion and Application Financial Support Policy", the new standard has a large decline in the field of private subsidies, but significantly increased the new energy taxi company Subsidy; Shanxi, Hunan, Jiangxi, Qingdao and other provinces and cities introduced charging infrastructure planning

- The rigor and refinement of subsidy standards will drive the transformation and upgrading of products. The subsidy standard for new energy vehicles was adjusted in April this year by the fact that some enterprises were cheated by inferior products during the market blowout process in 2015, and the subsidy standard was criticized as “heavy business and light privateâ€.

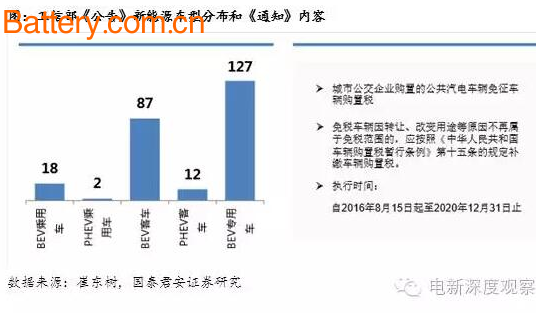

- The Ministry of Industry and Information Technology released the new vehicle product announcement for the "Road Motor Vehicle Manufacturing Enterprise and Product Announcement" (No. 287), and 246 new energy vehicles were selected; the Ministry of Finance and the State Administration of Taxation issued the "Regulations on the Acquisition of Public Steam Vehicles Exempted Vehicles by Urban Public Transport Enterprises" Notice of Purchase Tax.

- From this year on, the state replenishment funds will be cancelled, all of which will be liquidated afterwards, and the time period for grants will also become longer. In the future, the model of capping and capping of bicycle subsidies will be adopted, and a dynamic adjustment mechanism for subsidy standards linked to factors such as new energy production costs and sales scale will be established. When the amount of compensation from the applicant country exceeds the budget, the subsidy standards for various types of vehicles will be lowered proportionally.

- Although different organizations have different forecasts for new energy vehicles in the next five years, they are basically more than 1.1 million vehicles, accounting for about 2%-5% of the automotive market. The 16-year new energy vehicle is expected to sell 500,000-600,000.

Overview and prospects of lithium battery industry development

market Overview

- In 2016, China's 3C lithium battery market demand was 450 billion yuan, up 3.7% year-on-year. The market demand for power lithium battery was 60.5 billion yuan, up 65.8% year-on-year. In 2016, the number of power battery companies reached 145, and in 2017 it will reach 118, 2018. 85 years. In 2017, the integrated resources of power batteries began. No more than 50 after integration by 2020.

- The concentration of power lithium batteries in the East China region is completely different from that of digital battery companies. Reason: The automobile industry in East China has a good supporting capacity and strong capital strength. The battery manufacturers are also developing on the one hand with the help of local policies. From the perspective of industrial chain investment, the farther away from the central area, the easier it is to be marginalized.

- The price of lithium carbonate enters the bottoming process (the price of 10-12w is relatively reasonable); the price of wet diaphragm is generally stable.

- In 2015, China's lithium battery capacity was nearly 19GWH, and power accounted for more than 90%, but 10G capacity has not been released.

Technical route

- Whether it is ternary or lithium iron or lithium manganate, the time of technological transformation will be relatively short. In 11 years, everyone regards lithium iron phosphate as a gold mine. In the next 3-5 years, the ternary may be a better product, but after 5 years, his vitality may be attenuated again.

- There are two types of technical thresholds: (1) customer threshold, companies with stable customers (Samsung, ATL) will be more stable; (2) cost advantage (BYD, etc.), under the current possibility of large capital, this piece The profit will fall faster.

Lithium-ion power battery technology trends and industrial structure

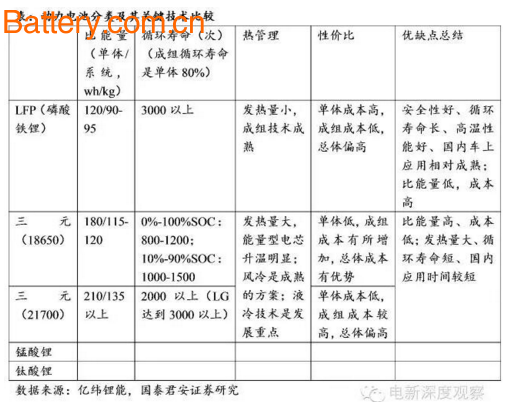

Power battery parameters, performance comparison

Key technologies for power batteries and systems:

- Specific energy. 18650 ternary cell specific energy density increase: 2.2-2.6-2.9-3.2Ah, specific energy density from 180 gradually increased 240Wh / kg.

- Consistency (materials, manufacturing processes, standardized products, large-scale production). It is roughly divided into static and dynamic consistency. Static consistency Currently, various classification methods can not meet the requirements of power battery consistency in nature. It is a static performance. After working for a period of time, especially at the end of life, it will produce large dispersion, and the life of the battery pack is shortened and safe. Not guaranteed. Dynamic consistency sorting is difficult, and there is no unified sorting standard in the industry, which is the focus of subsequent development.

- Cycle life. The ternary battery core (cylinder) improves the cycle life: (1) single cell cycle life: 2000 times or more; (2) fully automated production, guarantees the consistency of the cell core; (3) SOC use range: 10%~90% SOC (ie, charging to 4.15V, discharging to 3.0V).

- Thermal management. Divided into heating system and cooling system, according to different application areas, depending on the degree of environmental damage, the use of battery heating, select the appropriate cooling method.

- Safety and reliability. Includes battery, BMS, group connection, module mounting, plug and socket.

- Value for money. Focus on scale, standardization, and distribution power.

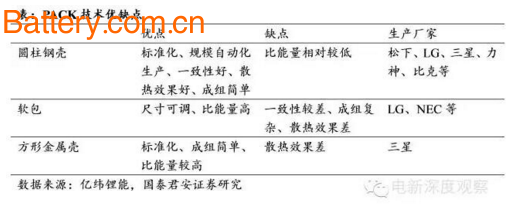

Battery pack technology. At present, the domestic ternary batteries are mainly 18650. In the next 2-3 years, with the maturity of pack technology and heat dissipation technology, the application of ternary batteries is mainly square.

18650 battery suitable for application scenarios

- Logistics vehicles: fixed driving range (100-150km), service life (3-5 years, 80-100,000km), use area (urban or urban-rural junction, better road conditions), less manned, low cost Turn.

- Special-purpose vehicles: fixed driving range, fixed daily usage time, and use area (city, road conditions are good).

- Passenger car: Meet the "Double 100", lightweight design, high specific energy, and sensitive to the price of the user.

Domestic and foreign market conditions

- Domestic policy: pure electric passenger car subsidies (2.5/4.5/5.5), plug-in hybrid passenger car (including extended program) subsidy 30,000; pure electric bus up to 500,000, plug-in hybrid maximum 250,000; special vehicles are divided into 1800 yuan / kwh, 1500 yuan / kwh, 1000 yuan / kwh three files.

- Domestic and international technical routes: Domestically, the square aluminum shell + LFP is mainly used in 2014. In 2015, the square aluminum shell + LFP+18650+ ternary parallel began, mainly used in low-end products such as special vehicles and mini-cars; Han) is based on the ternary system and is mainly used in medium and high-end products such as passenger cars.

- Domestic market size: In 2015, sales will be 350,000 units, corresponding to 17.5GWh; in 2016, it is expected to be 600,000 units, corresponding to 30GWh; in 2020, a total of 5 million units will be promoted, with an estimated 1.2 million units, corresponding to 60GWh.

The future development direction of power battery

- Lead acid battery: eliminated

- NiMH battery: on the edge of elimination, mainly used in hybrid vehicles

- Â Lithium-ion battery : 2016~2020, the main battery of the vehicle power supply

- Fuel cell: industrialization, it will take more than 10 years

- Material selection: Domestic, currently with lithium iron phosphate and ternary parallel mode, in the next 2 to 3 years, the ternary will occupy a larger proportion

- Cylindrical lithium-ion battery: 20700 will be the future

- Square lithium-ion battery: soft pack laminate and square aluminum shell parallel mode

Industry chain related manufacturers

- Pack: Beijing Pride; Haibo Sitron; Huasheng Power.

- BMS: Yi Neng, Kele, Ligao.

- Batteries:

- Materials: Cathode materials (Hunan Shanshan, Peking University, Hunan Ruixiang, Jinhe, Beijing Dangsheng), anode materials (Betray, Shanghai Shanshan, Hunan Xingcheng), electrolyte (new Zhoubang, Tianci, Guotai Huarong), diaphragm (Zhangzhou Mingzhu, Xinxiang Zhongke).

Ternary industry chain technology and market analysis

Policy Research

- Future subsidies will be transferred from ex-ante allocation to post-liquidation, which will have higher requirements for the company's financial strength, and the industry will accelerate integration.

- The new energy vehicle subsidy catalogue and access list are inconsistent and the scope of subsidies is smaller.

- Samsung and LG are unlikely to enter the fifth batch of power battery catalogs.

Market performance

- The price of the battery has dropped faster than the subsidy. The special car has not entered the catalogue and there is no specific plan. Therefore, for the logistics car company, the key is whether it can get the subsidy.

- The ternary materials are currently large, the price competition is fierce, the profit is low, and the lithium iron phosphate is relatively high. This year's total battery capacity is 29GWH, ternary 10GWH, and there will be a significant excess after the rapid release of production capacity at the end of 2016. However, structural problems remain outstanding, and high-end batteries are in short supply. It is expected that Sanyuan will reach 35GWH next year. Price: lithium cobalt oxide 18-19 million yuan, ternary 14-17 million yuan, lithium iron phosphate 100,000 yuan.

- Battery pack form. Cylindrical batteries are much cheaper than square and soft packs. For price-sensitive models such as logistics vehicles, the 18650 is the main type. The mainstream battery route is still square and soft package (mainly in terms of efficiency and weight), but because of the lack of a unified product system and low production efficiency, the price cannot be lowered. The cylinder is only a transitional choice at the current price.

opportunity

- The future opportunity is relatively large in the positive electrode material.

- The dominant position of car companies in the industrial chain is increasingly evident.

Electric vehicle battery system technology

Battery: Reliable (vibration, high and low temperature, electrical withstand), equalization (capacity, internal resistance, self-discharge).

BMS: PACK system fault detection and processing; system safety detection of smoke, fire, etc.; SOC, SOP, SOH; thermal equilibrium and thermal limit. The four aspects must meet the requirements, while the EV mode SOC error is less than 5%; the HEV mode SOC error is less than 10%. The development direction is hardware reliability, low cost, functional safety, vehicle integration and structural integration, software reliability, high precision battery state estimation.

If BMS manufacturers can form the BMS+PACK model in the future, and enter the core industry chain of car companies and battery companies, or gain industry competitive advantage.

Energy storage market outlook

Energy internet background

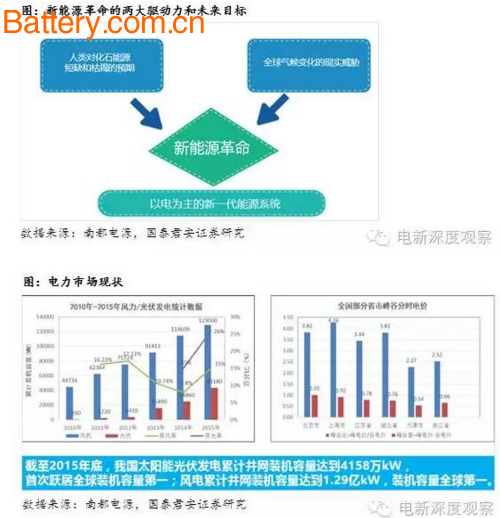

- China's energy and power are faced with the following characteristics: (1) The task of energy saving and emission reduction is arduous, the pressure is high (2) The energy structure is unreasonable, the resources are distributed away from the load center (3) The power generation capacity and load increase rapidly, but the Sanbei area “abandoned the wind†"Disposal of light" is a serious phenomenon of power curtailment. There is a huge imbalance between peak and valley electricity supply and demand in some provinces and cities. (4) Insufficient disaster prevention and risk response capabilities, low power supply reliability, and increasingly prominent power quality issues.

- After the new energy is connected, the grid faces four new problems, including (1) the grid is increasingly complex, the load is growing rapidly, and the load characteristics are more constant. The proportion of external power receiving in the load center is gradually increasing, and the problem of safety and stability is becoming more and more prominent. How to prevent large-scale power outages and ensure safe and stable operation of the power grid (2) Facing large-scale renewable energy (large-scale wind farms) and large-scale distributed power sources ( Access to solar energy , wind energy, gas turbines, electric vehicles , distributed energy storage; how the power grid handles coordinated operation with various types of renewable power sources, intermittent power supplies and heavy loads of loads (3) How to satisfy customers' reliable power supply to the power grid Increasing demands for power services such as sex and power quality (4) Facing the continuous improvement of the transparency of customer interface, meeting more flexible load demand, how the power company and users can cooperate more friendlyly, and realize the interaction between power grid and users. To achieve the purpose of improving operational efficiency, reducing electricity prices, and improving service levels. Therefore, the new mission of the grid under the new energy revolution has evolved into a new energy power transmission and distribution network and a flexible and efficient energy network, extremely high power supply reliability and integrated service system. In the new energy revolution, the energy Internet featuring “Internet + smart energyâ€, “marketization, decentralization, intelligence, and materialization†has become the core.

The value of energy storage in the energy Internet

The distributed energy storage system in the energy Internet is a necessary device for distributed energy access to traditional energy systems.

- With renewable energy connected to the grid, the intermittent power supply such as photovoltaics and wind power is unstable. When the proportion of power generation reaches a high proportion, it will have a certain impact on the power grid, so it needs a certain proportion of energy storage. Stabilize the output of wind power stations;

- Where the electricity price is higher than the on-grid price, the area where the price of the wave and valley is very different, the distributed supporting energy storage economy is good, and the demand for energy storage in the microgrid and off-grid is also very direct;

- Energy storage is applied to the power system to change the mode of simultaneous production, transmission and consumption of electric energy, introducing space and time factor elements into the power system, achieving two-way flow of power flow and flexibility of the power grid, and improving energy efficiency;

- Due to the large-scale access of renewable energy and distributed energy in large power grids, combined with the popularization of micro-grids and electric vehicles , the energy storage link will become a key node of the entire energy Internet.

- The electric power modification No. 9 document clearly stated that the grid power is positioned, the power generation market is developed, the electricity sales market is opened, and the distributed power generation on the user side is released. The energy storage market will usher in a blowout in 2024.

Energy storage business model

- The energy storage business has developed across the five-year period from battery to system to investment operation. There is a huge qualitative change in both market and technical capabilities and business models. The five key indicators of energy storage are cycle life, scale, safety, economy, and efficiency. Lead carbon energy storage technology can provide a ten-year life cycle and has an index advantage.

- Nandu Power's first "investment + operation" business model, similar to EPC (contract energy management), through the signing of energy-saving service contracts with customers, to provide customers with a complete set of energy-saving services, and recover from the energy-saving benefits obtained after customers carry out energy-saving renovation Investment and profit. The innovative business model will form an effective benefit distribution mechanism between investment entities such as client terminals and third-party energy storage enterprises, and energy storage industry funds, and accelerate the commercialization of energy storage. In the absence of the energy storage incentive policy, Nandu lead charcoal storage has already been commercialized on the user side. Through the peaking and valley filling of energy storage, the peak-to-valley electricity price difference according to the time-sharing electricity price policy can achieve the profit target, and on the basis of the power, the energy storage + value-added service income can be realized.

Interpretation of New Energy Vehicle Operation Industry Chain

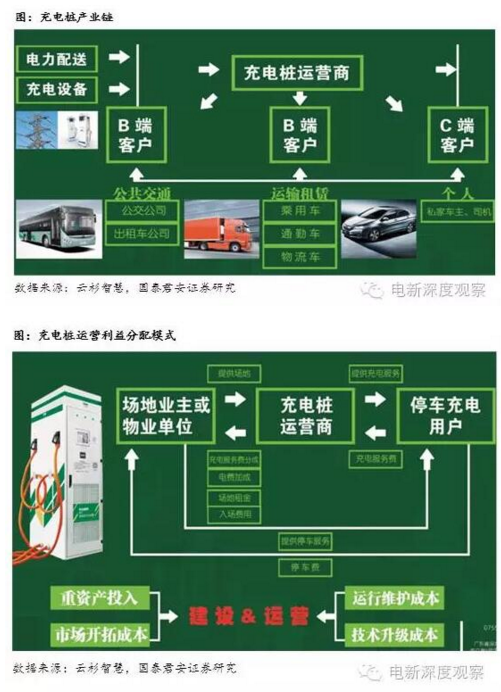

New energy vehicle industry chain overview

Charging pile operation

- According to the preliminary statistics of the National Energy and Energy Department, as of the end of June this year, 81,000 public charging piles have been built nationwide, an increase of 65% from the end of last year; more than 50,000 private charging piles have been built with vehicles, an increase of about 12% from the end of last year; From January to June, the national new energy vehicle charging capacity exceeded 600 million kWh; the number of related enterprises has exceeded 600. Charging piles are growing rapidly, but the increase in new energy vehicles is relatively lagging behind, mainly reflected in the B2C end. Compared with B2B, B2C's operating cost is low, but the income uncertainty is high, and external interference is also more (such as fuel truck occupancy, mobile phone can not calculate, power supply costs, etc.), the current profitability is worse than B2B. The low pressure utilization rate (the number of new energy vehicles is small, the charging pile can not form a network, the parking cost is expensive, the electricity is not full of electricity) and the double operating pressure (equipment cost, construction and installation cost, power operation cost) double pressure The profitability of the operating companies of the charging piles is difficult.

- Infrastructure-based operations currently have heavy assets (self-charging piles) and light assets (internet interfaces). The former is mainly characterized by a large number of self-operated charging facilities. Users need to apply for exclusive charging pile APP, which represents the company's national power grid, Putian, and spruce wisdom; the latter can only realize that users can find charging piles of different operators, and can not pay uniformly. .

New energy vehicle operations. There is no charging infrastructure to support, less charging pile construction (difficult to enter in hot areas), mismatched construction of outlets (less actual available charging piles), and disconnected charging piles. The competition in Beijing is fierce, Shanghai monopoly, new energy vehicles wait The overall market solution.

Analysis of the trend of electric logistics vehicle industry

Market size

- The total amount of social logistics in the country increased year by year from 2005 to 2015, of which the total social logistics in 2015 was 218.5 trillion yuan.

- Number of express delivery: According to the statistics of the State Post Bureau, in 2006-2015, China's express business volume CAGR reached 40%, from 1 billion in 2006 to 20.67 billion in 2015, an increase of nearly 20 times, and exceeded in 2014 for the first time. In the United States, the scale remains the first in the world.

- Express revenue: According to the statistics of the State Post Bureau, in 2015, China's express revenue reached 276.96 billion yuan, a year-on-year increase of 35.4%, an increase of more than 8 times compared with 30 billion yuan in 2006, and a CAGR of 28% in the past decade.

Industry pain point

- The new energy vehicle industry is relatively new and generally accepted, and the “car + pile + operation and maintenance†package is not perfect.

- Traffic management issues: The last mile of distribution in the first-tier cities, the use of electric tricycles, puts great pressure on the city's public road transport and social security.

- The development of the logistics industry is disorderly: At present, the logistics industry is huge, but the vicious competition is obvious, and the urban capacity mismatch is as high as 50%.

- The contradiction of road rights is prominent: Due to the continuous expansion of the city scale, there are many limited lines in the first and second tier cities, and the limit policy, especially for logistics vehicles (some cities choose to use passenger cars as logistics vehicles).

Ground-based iron operation mode: Main car rental business (long-term rental, short-term rental, time-sharing lease), providing vehicle services (customized vehicles, insurance annual review, maintenance, spare vehicles, on-site rescue, supporting facilities), system services (APP Application services, real-time vehicle positioning, battery power monitoring, optimized capacity services, charging services (electric pile protection, charging outlets, convenient payment). Determined to develop into the largest and most professional new energy vehicle operation service provider for urban logistics.

Concrete Pile Pre-stressed/Tension Machine:

Tension Machine is a kind of feedthrough pre-tensioing. It is also called Spun Pile tension jack machine, Pole Tension Machine, prestressed tension machine etc. It is the neccesary equipment to produce Pre-stressed Concrete Spun Pile and prestressed concrete pole products. As the end of the tension rod is connected to the anchor with thread, it can be applied to various forged anchors, chilled iron anchor used for stayed-cable bridge and other similar anchors, as well as pre-tension pulling for pipes. In accordance with actual requirement.

HH Tension Machine's advantages:

1. The large-screen LCD display.

2. Double control mechanism of touch screen and keyboard, high reliability.

3. Directly work after the input of tensioning data, and the oil cylinder will automatically complete the tensioning process to reduce uncertain factor of manual operations and improve the tensile quality.

4. Built-in SD card function, which can save the tensile data to the computer regularly, and check the record at any time.

5. With its own printer, it can print tensile data in working time, avoiding the tedious and unstable manual record and ensuring the traceability of tensegrity data is verified.

Technical Parameter:

1. Oil pump flow: 12L/min

2. Motor power: 7.5kw

3. Rated power: 31.5Kpa

4.Tension force: 2000KN

5. Tension stroke: 200mm

6. Programmable controller of automatic control system + input and output of analog data Color touch screen, USB interface output

7. Control voltage: 380V+24V

8. Accuracy of prestress control:±0.1Mpa

9. Data transmission rate is 100%

Main configuration:

Automatic tension control system, 300T jack, oil pump, lifting trolley, tensioning rod, tensioning head and supporting foot

If you have any questions, please contact with us. Welcome you can visit our Factory.For inqury,Please send mail directly to us.

Concrete Machine,Pre-Stressed Machine,Pre-Stressed Concrete Machine,Concrete Pre-Stressed Machine

Jiangsu Haiheng Building-Materials Machinery Co.,Ltd , https://www.jshaiheng.com